Bigger is Better as OJC mergers into FMCG Behemoth

How much juice can you squeeze out of an orange?

That’s what it has felt like for OJC shareholders that have been following the turnaround story of the company over the past three years.

But now, OJC is the centrepiece of a newly formed company that will generate $400M in revenue, $29M in EBITDA.

The new merged company will operate under the ticker of SPG and be worth around $280M at $1.50 (the current price for the raise).

This news has made headlines in the Australian mainstream media, given the significance of the brands involved and the personalities - including OJC Chairman Jeff Kennett.

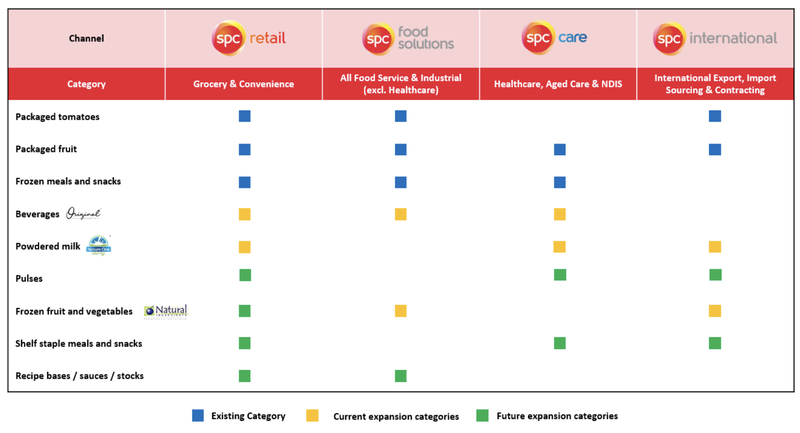

The merger is with three key brands OJC, SPC and Nature One Dairy.

These are the markets that the companies will now operate in:

For FMCG companies size matters, and economies of scale is the best way to reduce costs in the face of rising inflation.

Instead of three heads of procurement, the group will have one.

Instead of three boards of directors, the group will have one.

etc…

With companies that rely on economies of scale, Bigger IS Better.

For OJC this deal makes sense, as costs can now be absorbed into a bigger organisation with efficiencies improved across the business.

The key question is, was this a good deal for OJC shareholders?

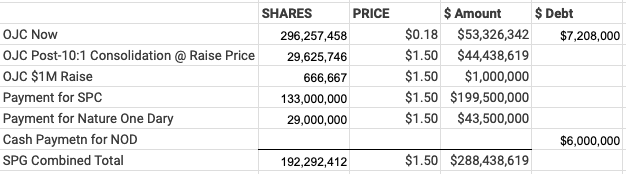

Post-consolidation, OJC will have around 15.5% of the total entity value.

Also, OJC will acquire Nature One Dairy and SPC “unencumbered”. Which means that OJC (and the new entity) will not take on the debt on their books.

After the 10:1 consolidation and $1M capital raise OJC’s market cap will be around $44M.

After the acquisitions and the raise the new SPG Company will be worth around $288M.

OJC’s share of this will be ~$44M - the same market cap post raise.

Here are our workings:

It is not totally clear what the total debt position of the business will be, however we expect more information to come to light before the vote in November.

In terms of price, OJC shareholders don’t get any immediate premium uplift in the value of the company, however we think that the value will be generated over time as synergies within the businesses improve.

All ships rise on a floating tide.

It also puts OJC in a position where larger funds looking to invest in Australian-based companies can now take a position given the conglomerates market size.

For these reasons we think that the merger is ultimately a good thing for the company and shareholders.

This sentiment is shared by the three largest shareholders of the company (that represent 42% of the vote).

Looking at the counterfactual - what would happen if OJC does not do the acquisition?

OJC would need to “grow it alone”.

Although the company, and CEO Steven Cail, have made excellent strides to strengthen the balance sheet of the business and reduce costs where necessary, it has faced many tailwinds in the last three years.

OJC at its core is a turnaround story.

However, since 2022 costs across the board have gone up.

Inflation hits every part of OJC’s business (energy prices, wage inflation, transport etc…).

But probably most challenging of all is that the price of oranges has gone up with poor crop yields in Brazil and Florida (orange juice futures were the highest increased commodity in 2023 - good for traders, bad for OJC).

The one saving grace for OJC was that inflation headwinds affected everyone in the industry, and it was a race to survive or be acquired.

This consolidated new venture will be a size and scale that means it can weather the inflation storm and potentially acquire smaller operators that can no longer survive in these conditions.

To grow the volumes needed to achieve economies of scale OJC would have likely needed to invest further in infrastructure…

That’s where SPC comes in.

SPC has facilities out in Shepperton that OJC can leverage to mitigate any “capacity limitations” for growth.

So, if OJC were to go it alone it would have been a long and hard journey of cost cutting, dilutionary capital raises and value destruction for shareholders.

Growth too would have also been challenging as further capital or debt would have needed to be raised in order to improve the capacity to make more products.

On the export front, going it alone would have been difficult too.

OJC would have needed to set up new relationships with suppliers overseas and developed “go to market” strategies that carry with it a ‘sales risk’.

Nature One Dairy brings this to the table.

The company has a big presence all throughout Asia, and we think that OJC can significantly benefit from the immediate inroads into this market:

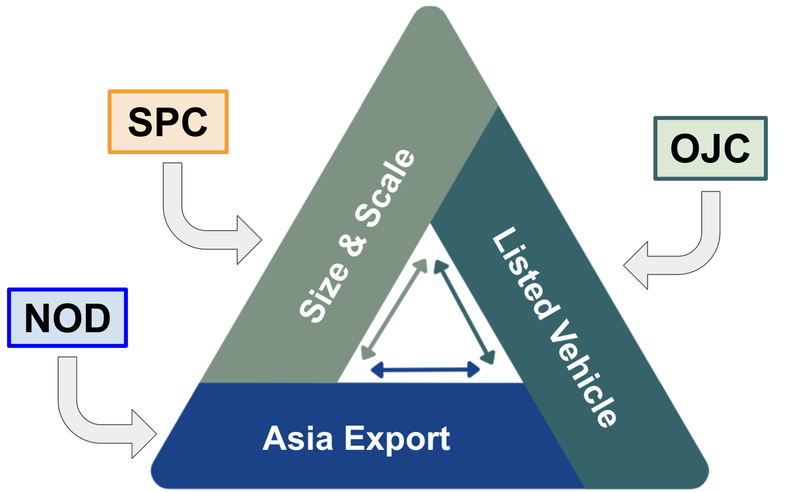

Although each company has their own brand and own story we think that this graph sums up the unique value that each company brings to the transaction:

Since taking over Steven Cail has only ever raised money once, through a $5M strategic investment from The Smith Family.

His ability to reduce costs across the business has put OJC in a strong position to support this merger.

It is unfortunate that the stars never aligned for OJC to properly see the fruits of its labour on its own - however in this bigger vehicle we think that it will give OJC the best chance to maintain a strong foothold in the FMCG market.

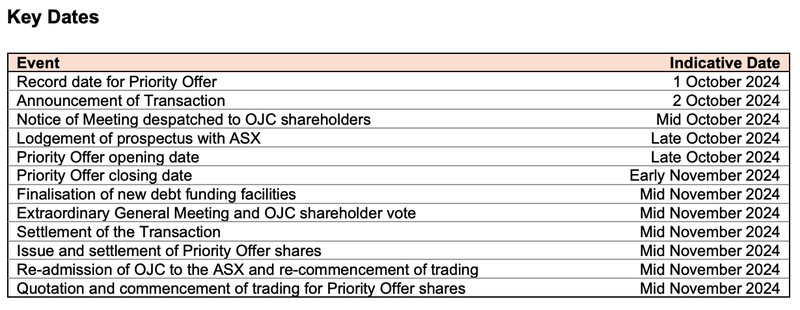

What is next for OJC?

The merger will be put to a vote for OJC shareholders.

It will also conduct a $1M priority raise from existing shareholders.